COLLATERALIZED VS. UNCOLLATERALIZED LOANS

First of all, mixing up “collateralized” and “uncollateralized” in finance is like mixing up Jon Snow and Tyrion Lannister when standing beside Kit Harrington and Peter Dinklage.

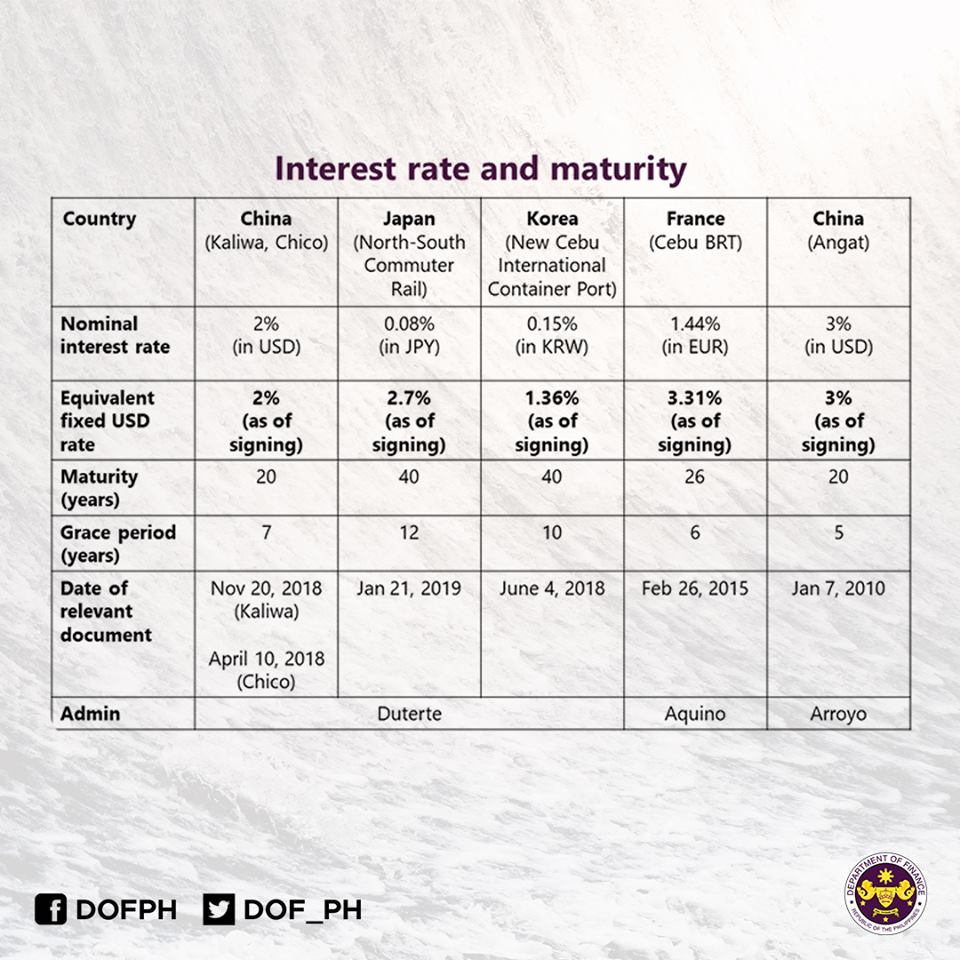

One can confirm that the US$62 million Chico River Pump Irrigation Loan (April 2018) and the US$211 million Kaliwa Dam Loan (November 2018), both from the Export-Import Bank of China, have no collateral. These relatively simple agreements (about 25 pages each, excluding annexes) can be downloaded from the Department of Finance website.

What is the difference between a “collateralized” and “uncollateralized” loan and why is it so basic that no first year finance lawyer or banker could possibly mix them up?

Collateral is familiar to us. If one does not pay a housing loan, the bank will foreclose on one’s house. If one does not pay an auto loan, the bank will repossess one’s car.

Simply, a loan has collateral when a borrower and a lender agree that if the loan is not paid, the lender may take specific property.

Because collateral radically changes a loan, it has to be very specifically written in — down to the specific title number of your land or the registration number of your car. Collateral is never automatic.

Try digging up your housing or auto loan. Look for the part that specifically refers to the specific title number of your land or the registration number of your car. If you signed a salary loan, look for the part allowing automatic deductions from your payroll bank account.

What happens if there is no collateral in the loan agreement?

Generally, if someone fails to repay a loan, the lender has to go to a judge. The judge must order the borrower to pay up.

If you signed an uncollateralized loan, such as a simple personal loan, and the bank suddenly takes your house because you failed to pay, the bank would be in big trouble and you would be the one suing the bank. The bank would be in such big trouble that no first year finance lawyer or banker would take someone’s house without collateral in the loan agreement.

Thus, if the lender wants to take the borrower’s house, the judge has to approve this, too.

Similarly, I cannot lend you P500 pesos and suddenly take your house when you forget to pay (unless you signed a loan agreement with collateral).

There is a big difference between being able to foreclose on a house in case of nonpayment — meaning, the bank is much more sure of being repaid — and having to go through the long process of suing a borrower in court. The difference is as big as the one between Jon Snow and Tyrion Lannister.