ADVERTISEMENT

Filtered By: Lifestyle

Lifestyle

Special Advertising Feature: Teaching kids how to save

+

Make this your preferred source to get more updates from this publisher on Google.

It is never too early to introduce to children the concept of saving for the future, but it can be a challenge. Focused only on the present, most of them would want to spend the money that they receive on the latest toys and gadgets. Thus, parents are faced with the task of teaching children why and how saving should be prioritized over spending.

The first lesson that kids should be taught is to identify work as the family’s primary source of funds. Without work, there would be no money to spend on priorities, such as food, clothes, rent or amortization and tuition fees. Since the monthly amount parents receive each month is limited, a portion of it should be saved while the rest must be wisely spent.

For young children, an actual piggy bank may be needed to introduce them to saving money. Whenever they receive cash during birthdays or Christmas, encourage them to place these inside a piggy bank. Parents can replicate this by having their own piggy banks at home. Offer to match whatever funds the kids save to further encourage them.

For young children, an actual piggy bank may be needed to introduce them to saving money. Whenever they receive cash during birthdays or Christmas, encourage them to place these inside a piggy bank. Parents can replicate this by having their own piggy banks at home. Offer to match whatever funds the kids save to further encourage them. As the piggy banks sit on the shelf for a while, take this opportunity to explain the value of having money for possible future needs like purchasing a new home appliance or getting a larger car for the family. These goals may be reinforced by a trip to the store or even pointing out a car on the street as it passes by.

Teens, meanwhile, can be given a weekly allowance which may be a way of introducing the concept of budgeting and looking after their funds responsibly.

After the importance of saving has been established, the children can be encouraged to open their own bank account, such as the PSBank Kiddie Account for children from 0-12 years old, and the PSBank Teen Savers Account for those 13-18 years old.

“We’re very happy to offer two new savings products that will be a good tool for parents to teach their kids the values of thrift, discipline and perseverance. We designed it in such a way that it would be very easy for parents to open and maintain the accounts. They don’t have to make an initial deposit and there is no maintaining balance which means their children can start saving even with a small amount. Their accounts also continue to earn interest regardless of the balance,” PSBank Business Development Division Head/Vice President Melissa Tong said.

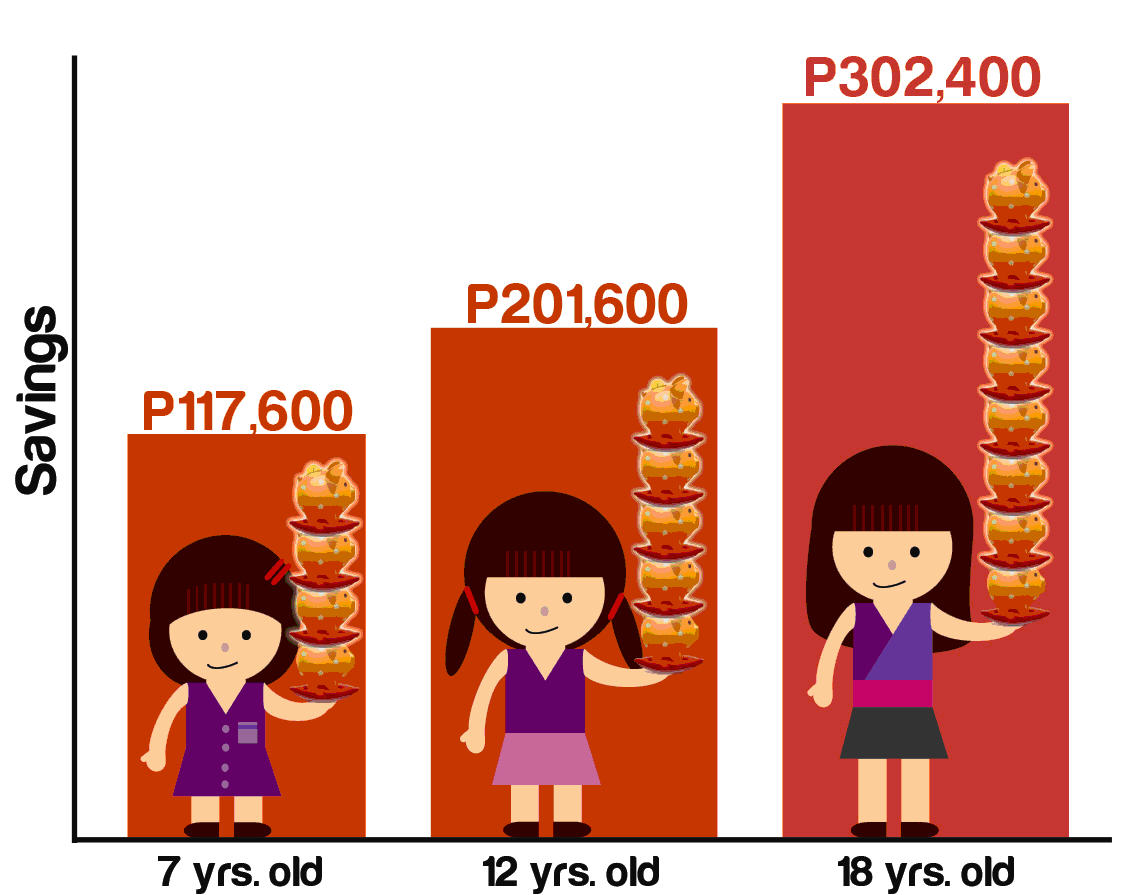

Imagine, if parents and kids set aside as little as Php 50 a day, they can accumulate up to Php 16,800 in a year (this does not yet include interest earnings). Do this and your kids can have a headstart by the time they go to college.

Imagine, if parents and kids set aside as little as Php 50 a day, they can accumulate up to Php 16,800 in a year (this does not yet include interest earnings). Do this and your kids can have a headstart by the time they go to college. For children below seven years of age, parents are advised to open an In Trust For (ITF) account. For those beyond seven years old, parents have the option of opening a joint or an individual account for each of their children.

To encourage the children further, the growth of their savings accounts can be monitored through PSBank Online, a 24/7 facility accessible via computer or tablet. As a bonus, the PSBank Teen Savers Account provides the child or teen account holder with a free personal accident insurance from Charter Ping An Insurance Corporation of up to five times the monthly average daily balance or a maximum of P500,000 per account (or a combined limit of P5 million per depositor).

For more details on the PSBank Kiddie and Teen Savers Accounts, parents or the kids’ generous aunts, uncles and godparents can call the Bank’s 24/7 hotline at (02) 845-8888 or visit their nearest PSBank branch. — Special Advertising Feature